China's economy resilient with potential and vitality

Chinese recovery won't be inflationary

By Chetan Ahya

The universal experience of re-opening an economy is a rise in inflation. What has been different across economies is the extent of the rise in inflation and its persistence. China's "reopening" has given rise to some natural questions: By how much will inflation rise in China? How persistent will it be? Will there be any significant spillover effects on the rest of Asian economies?

On Sunday, the Government Work Report set a GDP growth target of around 5 percent.

We (at Morgan Stanley) are more bullish than the consensus in expecting GDP growth to pick up to 5.7 percent in 2023. Yet, we also expect just a moderate uplift in China's core inflation, and headline inflation will remain well within the comfort zone of 3 percent because food prices continue to exert downward pressure.

This view is informed by the following perspectives.

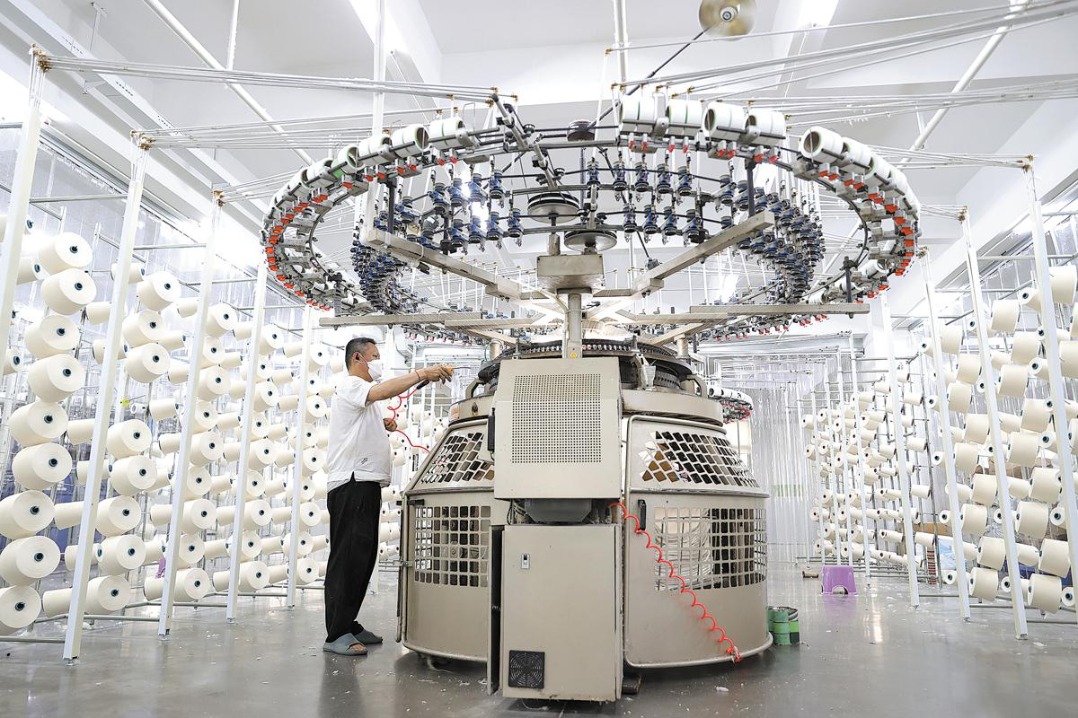

As the economy continues to "re-open" at a brisk pace, final consumption expenditure growth will accelerate. Within consumption, the acceleration will be driven more by an increase in spending on services as the continued relaxation in COVID-19 restrictions fueled the service sector's recovery. The services-led nature of the recovery means that goods translate to a relatively mild boost to goods prices and the non-commodity producer price index (PPI) given that the incremental demand will be driven more by services than goods.

There are concerns over China's consumption recovery and the reflation story potentially playing out like it did in the United States. However, the key difference is that the demand for goods in the US saw a significant rise because of the excess transfers to households, coupled with the fact that some restrictions were still in place in the US then.

Consumption growth in China too will be driven, to a certain extent, by excess household savings. But the excess savings have accumulated largely due to people's inability to spend amid prolonged, strict COVID-19 restrictions and precautionary savings because of the deteriorating labor market conditions, rather than from transfers.

Furthermore, manufacturing capacity utilization ratios fell in 2022, and we believe there will be room for them to pick up before they get to a point where there will be significant upward pressures on goods inflation.

The fact that we expect recovery in China means unemployment rates will decline while wage growth will pick up from a cyclical perspective. However, as labor market dynamics have not been distorted by excessive transfers, we don't see labor participation rates being held back as the recovery progresses.

Moreover, the ongoing slowdown in exports will also help to cap overheating pressures in the labor market as hiring trends would be slowing in the manufacturing sector.

As for the spillover effects on the rest of Asia, we think that two transmission channels matter the most.

First, an increase in demand from China would raise oil and non-oil commodity prices. For oil prices, the key will be the extent of the improvement in mobility and international travel. But the impact will be mitigated by a more subdued backdrop for industrial and construction activity. For non-oil commodities, the outlook for infrastructure and property spending is key as they are the main sources of demand, and we expect only a moderate improvement in combined spending growth in the infrastructure and property sectors this year.

In past cycles, investments helped drive China's recovery in the initial parts. This led to pronounced spillover effects as the capex-led recovery accelerated the rise in commodity demand and prices. The recovery in investment, however, is more moderate in this cycle.

While policymakers have initiated policy easing to boost infrastructure spending as they usually did during past cycles, a key difference is how the demand for commodities from the property sector is faring. Policymakers are now trying to stabilize the housing market, seeking to improve liquidity conditions of developers and relax the purchase restrictions which were imposed when the market was overheating.

As for infrastructure, we expect the policymakers to counter-cyclically reduce the increase in infrastructure spending given the need to conserve fiscal space. The overall fixed asset investment growth will increase to 4.5 percent in 2023 from 2.4 percent in 2022. Within that what matters most for the non-oil commodity demand is the expenditure on infrastructure, which is expected to rise from 0.7 percent in 2022 to 2.8 percent this year.

Second, since China is the largest supplier of goods to the rest of Asia, inflation pressures may pass from China's goods prices to the region's import prices and further to its consumer price index. But what matters more is the global goods demand/supply balance. And the still deflating global goods demand will further limit any spillover effects on the region's inflation.

We expect disinflation to continue in Asian economies. Our base-case forecasts are more dovish than those projected by others as we believe that inflation for 90 percent of the economies in Asia would have returned to the central banks' comfort zones by the middle of the year.

The author is chief Asia economist, Morgan Stanley. The views don't necessarily reflect those of China Daily.